At least consider a shorter one

Affordability and stability are reasons homebuyers choose a 30-year fixed rate mortgage. It makes the payment lower than a 15-year mortgage and the principal and interest portion of the payment will be constant for 30 years. |

A common belief among homeowners for decades was that they would always have mortgage payment. The Great Recession has caused many individuals to rethink that concept and make plans to get their home paid for sooner.

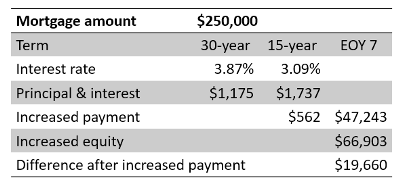

For people who can afford it, shorter term mortgages will provide a lower interest rate and build equity faster. A 3.09% 15-year fixed-rate mortgage compared to a 3.87% 30-year loan will have a $562.42 higher payment.

The equity would be $66,903.04 greater on the 15-year term at the end of seven years. Even after you consider the higher payment on the shorter term, the equity difference is still almost $20,000 greater.

By choosing a 15-year loan, a borrower is committing to the higher payment for the term of the mortgage in exchange for a slightly lower interest rate. Another approach would be for the borrower to acquire a 30-year mortgage and make payments as if it were on a 15-year term. The slightly higher rate would allow the borrower the flexibility of not having to make the higher payment in the event he could not afford it on any particular month.